Arm Holdings (ARM) has entered 2026 at a historic inflection point, trading near $140 as it solidifies its position as the foundational architecture powering the majority of the world's mobile, edge, and increasingly AI-enabled devices. With Armv9 adoption accelerating across smartphones, data centers, PCs, automotive, and AI accelerators, Arm Holdings (ARM) is transitioning from a mobile-centric IP licensor to central architecture underpinning the AI and intelligent computing era. Explore the institutional price targets, the licensing roadmap, and whether ARM is a buy in 2026.

In early 2026, Arm Holdings (ARM) has decoupled from traditional mobile cycles. While smartphone royalties remain a reliable base, growth in cloud, automotive, PC, and AI workloads has fueled unprecedented royalty acceleration. As of March 2026, the narrative centers on Armv9 penetration, AI-specific IP licensing, and royalty rate expansion. Arm Holdings (ARM) enters 2026 with massive structural tailwinds. CEO Rene Haas continues to emphasize Arm's central role in AI and intelligent computing, projecting sustained double-digit royalty growth and significant margin improvement. With record design wins and ecosystem expansion, 2026 shapes up as a pivotal year.

This guide breaks down the Arm Holdings (ARM) stock price prediction for 2026 using data from analysts and consensus estimates. You will also discover how to gain exposure to Arm Holdings (ARM) stock futures through BingX TradFi.

Read more: Ferrari N.V. (RACE) Stock Outlook for 2026: Can An Iconic Brand and EVs Drive RACE Stock to $550+?

Top 5 Things for Arm Holdings (ARM) Investors to Know in 2026

- Armv9 Adoption Surge: Armv9-based chip shipments grew over 50% year-over-year in 2025, with strong momentum in premium smartphones, data centers, and AI edge devices.

- Royalty Rate Expansion: Average royalty rates increased meaningfully due to mixed shifts toward higher-value IP and AI-specific licenses.

- Revenue Momentum: FY2025 revenue reached approximately $3.8 billion, up 25% YoY, driven by royalty growth and licensing deals.

- Polarized Targets: Analyst forecasts for 2026 range from bearish lows around $90 to bullish highs of $250 to $280.

- Valuation Debate: Forward P/E around 70-80x reflects AI growth premium, but royalty scalability and ecosystem moat support continued re-rating.

What Is Arm Holdings (ARM)?

Arm Holdings (ARM) is the world's leading semiconductor IP company, designing processor architectures used in over 99% of smartphones and a rapidly growing share of data centers, PCs, automotive, IoT, and AI devices. In 2026, it is increasingly classified as the foundational architecture for AI and intelligent computing. Its core value lies in royalty-based licensing, low-power efficiency, and ecosystem dominance. Unlike fab-based chipmakers, Arm Holdings (ARM)'s ecosystem includes thousands of licensees, vast software compatibility, and a business model with high gross margins and excellent scalability.

Arm Holdings (ARM)'s Strategic Evolution (1990-2026): From Mobile to AI Architecture Leader

Founded in 1990, Arm Holdings (ARM)'s history features transformative milestones. Early success in low-power mobile processors led to dominance in smartphones. The 2016 SoftBank acquisition accelerated global expansion. Recent years have focused on Armv9, AI-specific extensions, and data center penetration. From mobile roots to AI architecture leadership, Arm Holdings (ARM) has consistently adapted to computing shifts.

Arm Holdings (ARM)'s Key Growth Phases Over the Years: From Mobile to AI Dominance

Arm Holdings (ARM)'s journey spans distinct eras:

- Mobile Phase (1990-2015): Dominating smartphone processors.

- Diversification Era (2015-2022): Expanding into servers, automotive, and IoT.

- The AI & Data Center Era (2023+): Armv9 and AI extensions driving hyper-growth.

Arm Holdings (ARM) 2025 Performance Overview: The Royalty Acceleration Year

In 2025, Arm Holdings (ARM) navigated a stabilizing mobile market while experiencing accelerating royalty growth from non-mobile segments, particularly data centers, edge AI, premium smartphones, automotive, and IoT. While smartphone royalties remained the largest contributor and provided baseline stability, Armv9 architecture adoption surged across high-value devices, driving meaningful royalty rate expansion and ecosystem momentum. Massive investments in AI-specific IP extensions, automotive-grade architectures, and data center solutions fueled rapid design wins and license agreements.

This powerful combination of reliable mobile royalty base and explosive growth in cloud, edge, and AI workloads produced record financial results, with royalty revenue reaching new highs and operating margins benefiting from the highly scalable licensing model, though R&D spending remained elevated to support next-generation architecture development.

Read more: What Is TradFi (Traditional Finance) On-Chain: A Beginner's Guide

1. ARM Stock Performance, Market Cap Crosses $140B

Arm Holdings (ARM)'s stock exhibited strong and sustained upward momentum throughout 2025, driven by accelerating royalty reports, AI ecosystem enthusiasm, and investor recognition of Arm's central role in intelligent computing. Shares achieved multiple all-time highs during the year, with market capitalization consistently surpassing $140 billion and peaking near $170-$180 billion following particularly strong quarterly royalty updates and design-win announcements. Volatility was moderate compared to broader semiconductor peers, with the stock maintaining elevated forward multiples that reflected Arm Holdings (ARM)'s royalty scalability, ecosystem dominance, and long-term AI/edge penetration, while significantly outperforming most semiconductor indices in key periods.

2. Financial Performance: Revenue $3.8B, Up 25% YoY

Arm Holdings (ARM) delivered robust and accelerating growth, with full-year revenue reaching approximately $3.8 billion, up 25% year-over-year. Royalty revenue grew significantly faster than overall revenue, driven by Armv9 penetration in premium smartphones, data center CPUs, and edge AI devices. Licensing revenue also increased meaningfully due to new AI-focused agreements and higher-value contracts.

Operating margins remained exceptionally high due to the royalty-heavy, capital-light business model, with gross margins consistently in the mid-90% range. Net income and diluted EPS grew strongly, supported by operating leverage and disciplined expense management. Quarterly results showed clear acceleration, particularly in Q3 and Q4, as non-mobile royalties ramped rapidly.

3. Armv9 & AI Surge: Growth Exceeds 50%

Armv9-based chip shipments grew over 50% year-over-year in 2025, with strong momentum in premium smartphones, data center processors, AI edge devices, and automotive applications. Royalty rates expanded meaningfully due to mixed shifts toward higher-value IP, AI-specific extensions, and increased licensing of advanced architectures.

Data center royalty contribution increased significantly, reflecting the growing adoption of Arm-based CPUs in cloud and AI workloads. This performance underscored Arm Holdings (ARM)'s successful positioning as the preferred architecture for energy-efficient, high-performance computing across mobile, cloud, edge, and automotive.

4. Strategic Milestones: Ecosystem Expansion and AI Focus

Arm Holdings (ARM) secured additional high-value AI and data center licenses, expanded partnerships with hyperscalers, PC OEMs, and automotive OEMs, and advanced Armv9-based IP for next-generation edge AI and automotive applications. The company continued heavy investment in AI-specific architecture extensions, security features, and automotive-grade solutions.

Ecosystem momentum accelerated with growing software support and developer tools for Arm-based AI platforms. Arm Holdings (ARM) also maintained disciplined capital return through dividends and selective buybacks, reflecting strong cash flow generation from the royalty model.

Read more: PepsiCo (PEP) Stock Outlook for 2026: Can PEP Cross $220 on Beverage Portfolio and Emerging Markets?

The Arm Holdings Thesis for 2026: 5 Pillars of $ARM Stock Valuation

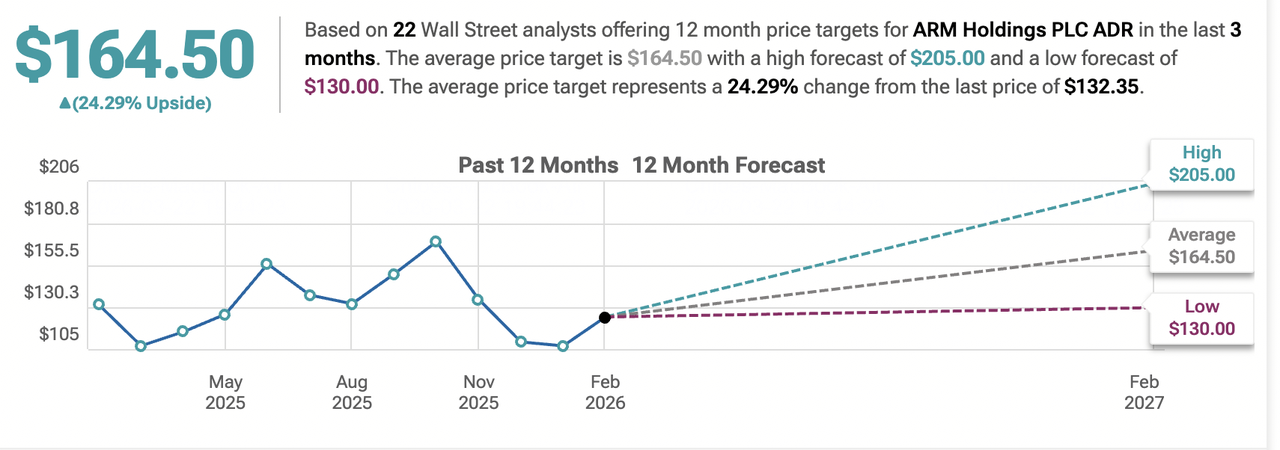

Arm Holdings Stock Projections Source: TipRanks

While mobile royalties continue to provide reliable baseline revenue, Arm Holdings (ARM)'s valuation in 2026 overwhelmingly reflects its central role as the foundational architecture for the intelligent computing era, with Armv9 adoption, AI-specific IP, and royalty scalability driving the majority of incremental growth and upside potential.

1. Armv9 Adoption: The Core Growth Pillar

Armv9 architecture penetration across premium smartphones, data centers, edge AI devices, and automotive applications drives sustained double-digit royalty growth. As more high-value chips transition to Armv9, royalty rates expand due to richer feature sets and higher ASPs, creating powerful revenue leverage.

2. AI-Specific IP and Extensions: The High-Growth Pillar

Arm Holdings (ARM) continues to license AI-optimized extensions, vector processing capabilities, and specialized IP for edge inference, cloud AI, and automotive AI workloads. These higher-value licenses generate outsized royalty rates and attract new licensees in fast-growing AI segments, fueling accelerated royalty revenue and ecosystem stickiness.

3. Royalty Scalability and Operating Leverage: The Profitability Pillar

Arm Holdings (ARM)'s business model features extremely high gross margins (mid-90% range) and low incremental costs as chip volumes scale. As Armv9 and AI IP adoption accelerates across billions of devices, royalty revenue compounds with powerful operating leverage, driving significant EPS growth and margin expansion without proportional cost increases.

4. Ecosystem Moat and Software Compatibility: The Defensive Pillar

Arm Holdings (ARM)'s vast software ecosystem, developer tools, and compatibility across billions of devices create formidable switching costs for licensees. Once a chip designer adopts Arm architecture, the cost of migrating to alternatives (RISC-V or proprietary) is extremely high. This moat ensures long-term royalty visibility and protects against near-term competitive displacement.

5. Diversified End Markets and Royalty Visibility: The Stability Pillar

Exposure across mobile, data center CPUs, edge AI, automotive, IoT, and emerging markets provides multi-year royalty visibility and reduces dependence on any single segment. Growing contributions from high-ASP data centers and automotive chips diversify revenue and support consistent royalty growth even during mobile cycle softness.

Read more: Marvell (MRVL) 2026 Outlook: Can AI & Silicon Momentum Drive Stock to $150?

Arm Holdings (ARM) Price Forecasts for 2026: Bull vs. Bear Outlook

Institutional views on Arm Holdings (ARM) stock remain polarized, balancing powerful royalty acceleration against mobile cyclicality and competitive threats.

| Platform | Type | Advertised Fee | Hidden/Other Costs | True Cost (Approx. Total) | Best For |

| BingX | CEX | 0.1% ($1.00) | 0.01% Spread ($0.10) | $1.10 | Lowest overall cost & transparency |

| Binance | CEX | 0.1% ($1.00) | 0.01% Spread ($0.10) | $1.10 | High liquidity, BNB discounts |

| OKX | CEX | 0.2% Taker ($2.00) | 0.02% Spread ($0.20) | $2.20 | Competitive fees for makers |

| Kraken (Pro) | CEX | 0.26% Taker ($2.60) | 0.02% Spread ($0.20) | $2.80 | Advanced users |

| Coinbase (Simple) | CEX | 1.49% ($14.90) | 0.5% Spread ($5.00) | $19.90 | Absolute beginners (at a high cost) |

| Robinhood | CEX | 0% | 0.8% Spread ($8.00) | $8.00 | Users unaware of hidden fees |

| Uniswap | DEX | 0.3% ($3.00) | $25+ Gas Fee | $28.00+ | Self-custody & DeFi natives |

Source: Aggregated from MarketBeat, Yahoo Finance, and analyst reports (as of early March 2026)

The wide range from bullish targets above $250 to bearish calls below $130 captures uncertainty around royalty acceleration, mobile cycles, and competitive dynamics.

The Bull Case: The AI Surge Drives ARM Stock Price Above $250

Bulls focus on Armv9 adoption and AI-specific IP momentum. If Arm Holdings (ARM) sustains double-digit royalty growth across mobile, data center, edge AI, and automotive, secures additional high-value licenses, and benefits from ecosystem expansion, the company could achieve strong revenue growth, margin leverage, and multiple expansion. This positions Arm Holdings (ARM) as the foundational architecture for intelligent computing, supporting targets of $250 or higher by year-end 2026.

The Bear Case: The Correction to $130 or Lower

Bears highlight mobile cyclicality and competitive threats. If smartphone shipments weaken significantly, RISC-V adoption accelerates, or licensee negotiations pressure royalty rates, multiples could compress sharply. Execution risks would drive the share price lower, with some targets in the $90 to $130 range.

Long or Short Arm Holdings (ARM) Stock Futures with USDT on BingX TradFi

Arm Holdings stock perpetuals on the futures market with BingX AI insights

For active traders looking to capitalize on high-volatility events like earnings reports, BingX TradFi offers advanced margin trading.

- Go to the BingX TradFi section and select Stock Futures.

- Locate the ARM/USDT perpetual contract.

- Choose your Margin Mode (Isolated or Cross) and set your Leverage (typically 2x-5x is recommended for equities).

- Analyze the trend and select Open Long if you expect a price increase or Open Short to profit from a decline.

- Set your Take-Profit (TP) and Stop-Loss (SL) levels immediately to manage risk against 2026's aggressive price swings.

5 Critical Risks to Watch for Arm Holdings (ARM) Traders in 2026

While Arm Holdings (ARM)'s foundational architecture dominance, rapid Armv9 adoption, and accelerating royalty growth from AI, data center, edge, and premium mobile devices offer substantial upside through ecosystem scalability and royalty leverage, traders must navigate a complex landscape of mobile cyclicality, competitive architecture threats, licensee negotiation risks, geopolitical exposure, and valuation concerns.

1. Mobile Market Cyclicality and Smartphone Demand Sensitivity

Arm Holdings (ARM) still derives the majority of its royalty revenue from smartphones. A prolonged slowdown in global smartphone shipments, delayed refresh cycles, or reduced demand for premium devices in 2026 could materially pressure royalty growth. Even though data center and automotive royalties are growing rapidly, any significant weakness in the mobile segment (which remains the largest contributor) would offset gains elsewhere and expose the stock to meaningful downside, especially given the high valuation that prices in continued acceleration across all end markets.

2. Competitive Pressure from RISC-V and In-House Architectures

RISC-V, the open-source instruction set architecture, is gaining traction among hyperscalers, IoT companies, and emerging chip designers. Major players, including Nvidia, Qualcomm, Google, Meta, and others, have invested in RISC-V or in-house custom architectures that could reduce reliance on Arm Holdings (ARM) IP over time. If RISC-V adoption accelerates in data centers, edge AI, or automotive, or if key licensees shift toward proprietary designs, Arm Holdings (ARM) royalty growth could moderate, eroding market share and long-term growth assumptions in high-value segments.

3. Licensee Negotiation and Royalty Rate Risks

Arm Holdings (ARM)'s business model depends on licensing agreements with thousands of chip designers. Renewals, renegotiations, or disputes with large licensees (Qualcomm, Apple, Samsung, MediaTek, etc.) could result in lower royalty rates, capped growth, or loss of exclusivity in certain categories. Any material adverse outcome in high-profile negotiations or legal challenges over licensing terms would directly impact royalty revenue and investor confidence in the sustainability of Arm Holdings (ARM)'s royalty rate expansion.

4. Geopolitical, Trade, and Supply Chain Risks

Arm Holdings (ARM) is exposed to geopolitical tensions, particularly U.S.-China trade restrictions, export controls on advanced semiconductor technology, and potential sanctions affecting licensees or ecosystem partners. Any escalation that limits Arm Holdings (ARM) IP usage in China (a significant market) or disrupts global chip supply chains could reduce royalty revenue from affected customers. Regulatory changes in key markets (e.g., data sovereignty rules, antitrust scrutiny of licensing practices) would also create headwinds for Arm Holdings (ARM)'s global licensing model.

5. Macro and Semiconductor Cycle Risks

Arm Holdings (ARM)'s royalty revenue is indirectly exposed to broader semiconductor industry cycles through its licensees' chip shipments. A global semiconductor downturn, reduced consumer electronics spending, or inventory corrections in mobile, PC, or IoT could cause royalty growth to slow or turn negative temporarily. While data center and automotive provide diversification, macro weakness would still impact overall royalty trends and earnings visibility, especially given the stock's elevated valuation that assumes continued acceleration.

Read more: Eli Lilly (LLY) Stock Outlook 2026: Can Mounjaro and Zepbound Momentum Drive LLYON Stock to $1,200+?

Conclusion: Should You Invest in Arm Holdings (ARM) Stock in 2026?

Deciding whether to invest in Arm Holdings (ARM) in 2026 requires viewing it as a high-conviction play on the future of intelligent computing and AI-enabled devices rather than a pure mobile royalty story. For growth-oriented investors with tolerance for cyclicality and competitive risk, Arm Holdings (ARM)'s Armv9 penetration, rapid expansion into data center, edge AI, automotive, and premium mobile, combined with royalty scalability and ecosystem dominance, support significant upside if royalty growth continues across multiple end markets. Successful execution on AI-specific IP and ecosystem expansion could drive substantial returns and multiple expansion.

For conservative or risk-averse investors, the stock's dependence on smartphone cycles, intensifying RISC-V and in-house architecture competition, licensee negotiation risks, geopolitical exposure, and premium valuation leave little margin for error. The performance now ties to multiple key drivers: either Arm Holdings (ARM) sustains royalty acceleration across mobile, cloud, edge, and automotive to justify the multiple, or mobile weakness, competitive displacement, or external pressures trigger sharp compression toward historical averages. Closely monitor quarterly royalty revenue trends, Armv9 shipment penetration, data center royalty contribution, design-win announcements, and global smartphone/PC/automotive demand indicators as the clearest signals of whether Arm Holdings (ARM) can maintain its position as the foundational architecture for the intelligent computing era in 2026.

Risk Reminder: Trading and investing in equities like ARM involves substantial risk of capital loss. Arm Holdings (ARM)'s high valuation, cyclical mobile exposure, competitive threats from RISC-V, and dependence on licensee adoption make it a high-risk asset. Investors should conduct thorough independent research and consider professional financial advice before allocating capital.

Related Reading

- Circle IPO (2025) Everything You Need to Know About CRCL, Valuation, What It Means for Crypto Market

- Strategy (MSTR) Stock Outlook 2026: Can MSTR Cross $700 on Bitcoin Treasury Strategy?

- Robinhood Stock Forecast 2026: $130 Hyper-Growth or Valuation Correction?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- What Are Coinbase Tokenized Stocks COINX and COINON and How to Buy Them?